How to Find a Lost 401(k)

Fortunately, retirement savings rarely disappear. Even if your former employer closed, merged with another company, switched investment providers, or automatically rolled your account into an IRA, there are usually records that can help you locate your money. In some situations, retirement funds may even end up with a state’s unclaimed property program. This guide walks through every major place to search so you can confidently begin your recovery.

Most Lost 401(k)s Can Be Found—If You Know Where to Look

The key is understanding that there isn’t just one place to search. Finding a lost retirement account often means checking several sources—including former employers, retirement plan administrators, financial institutions, government databases, and state unclaimed property programs. The more complete your search, the better your chances of recovering every dollar you’ve earned.

In This Guide

- Find forgotten retirement accounts

- Search former employers and plan administrators

- Locate automatic rollover IRAs

- Use official government databases

- Check state unclaimed property programs

- Search on behalf of a deceased family member

Finding an Old 401(k)

Why Retirement Accounts Become "Lost"

In fact, many people don’t realize they have more than one retirement account. Every employer-sponsored 401(k), 403(b), or similar workplace retirement plan creates another account that must be managed separately unless you actively combine or roll it over.

Common Reasons a 401(k) Becomes Difficult to Find

Common reasons include:

- Changing employers and forgetting about an old account.

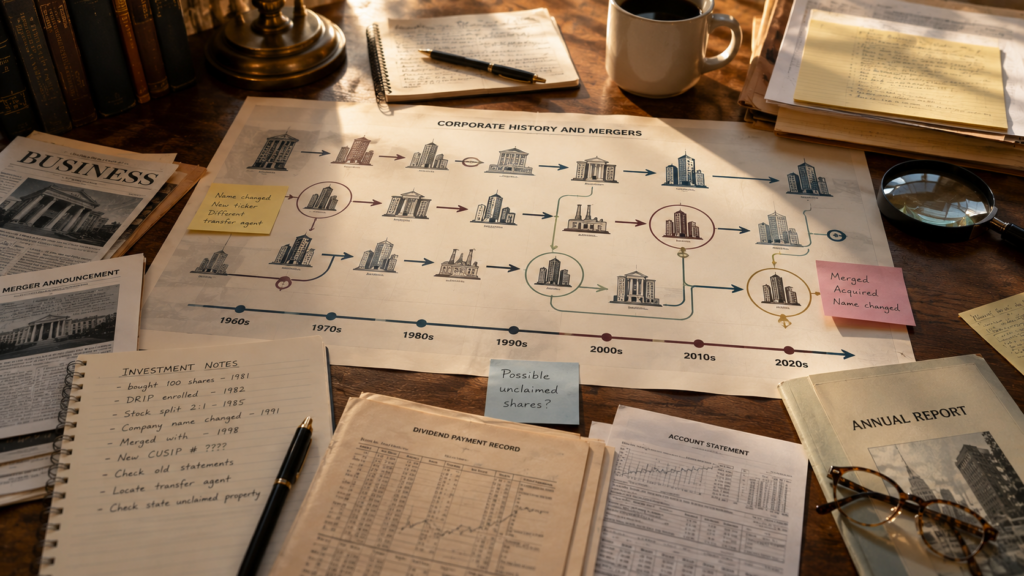

- Your employer merged with or was acquired by another company.

- The retirement plan administrator changed.

- Your employer changed investment companies.

- Your account was automatically rolled into an IRA after leaving employment.

- You moved without updating your mailing address.

- You stopped receiving statements or emails.

- You changed your name after marriage or divorce.

- Your employer went out of business.

- You’re helping locate retirement savings after a family member passed away.

Where Your Retirement Money May Be Today

Depending on your circumstances, your retirement savings may still be held by your former employer’s retirement plan, a new plan administrator, a financial institution that received an automatic rollover, a successor company following a merger or acquisition, or, in limited circumstances, a state’s unclaimed property program. Understanding these possibilities helps you search more efficiently instead of focusing on only one source.

Possible Places Your 401(k) Could Be

- Former employer names

- Current plan administrator

- Recordkeeper

- Automatic rollover IRA

- Successor company after a merger

- Financial institution

- State unclaimed property office

- Inherited retirement account records

Did You Know?

Step-by-Step Guide to Finding a Lost 401(k)

Build Your Employment Timeline

Old W-2s, tax returns, employee handbooks, onboarding paperwork, and pay stubs often contain valuable clues that can point you toward the correct retirement plan.

Review Your Financial Records

Don’t overlook old filing cabinets, digital cloud storage, or boxes in storage. Retirement paperwork often survives long after people forget opening the account.

Contact Your Former Employer

If the company merged or changed names, research the successor organization before assuming the account is gone.

Search Beyond Your Employer

You should also search official government retirement resources and your state’s unclaimed property office, since some retirement-related funds may eventually be reported as unclaimed property depending on state law and the type of distribution involved.

Expand Your Search If Necessary

Keeping detailed notes of every organization you contact prevents duplicate work and makes it easier to follow up if additional documentation is requested.

Common Reasons People Lose Track of a 401(k)

I Changed Jobs Years Ago

My Employer Went Out of Business

The Company Changed Names or Merged

I Think My Account Was Rolled Into an IRA

I'm Searching for a Parent's or Spouse's Retirement Account

I Think the Money Became Unclaimed Property

Expert Tips for Finding Forgotten Retirement Savings

Create One Master Employment List

Write down every employer you've worked for, including seasonal jobs, part-time positions, internships, and companies that no longer exist. Even short periods of employment may have resulted in retirement plan participation.

Search Under Previous Names

If you've changed your name because of marriage, divorce, or another legal reason, remember that older retirement accounts may still be associated with your previous name. Be prepared to provide documentation if requested.

Don't Ignore Small Account Balances

Many people assume an account with only a few hundred dollars isn't worth finding. However, investment growth over many years can significantly increase its value, and multiple small accounts can add up to meaningful retirement savings.

Keep Detailed Notes

Record every phone call, email, website search, and organization you contact. Include dates, reference numbers, and the names of representatives you speak with so you can easily follow up if additional information is needed.

Verify Beneficiary Information

Once you locate an account, review the listed beneficiaries and update them if necessary. Many people overlook this important step after marriage, divorce, or the birth of children.

Consolidate Accounts Carefully

Finding a forgotten 401(k) is only the first step. Depending on your financial goals, it may make sense to leave the account where it is, roll it into your current employer's retirement plan, or transfer it into an IRA. Consider speaking with a qualified financial professional before making major retirement decisions.